Budget 2026: a small win for taxpayers

By Nicci Courtney-Clarke · Updated

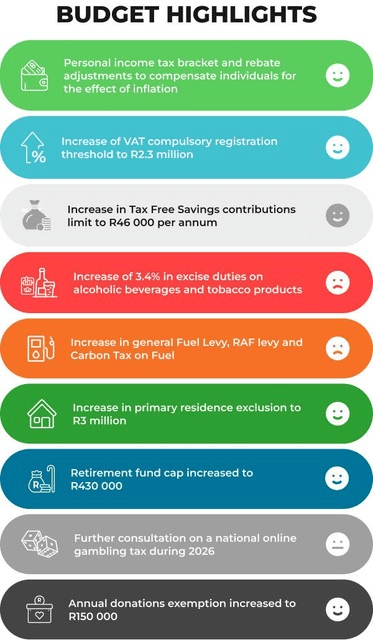

Finance Minister Enoch Godongwana delivered some welcome relief for taxpayers in the 2026 Budget, with inflationary adjustments to personal income tax brackets and medical tax credits helping to ease the impact of bracket creep after two years of no changes. There are also some meaningful wins, including a higher CGT exclusion on primary residences and increased thresholds for small business regimes.

Importantly, a proposed R20 billion in additional tax increases has been scrapped, softening what could have been a much tougher budget. However, it’s not all good news. Fuel levies are rising, and inflation-linked increases to alcohol and tobacco duties mean everyday costs will still edge higher — leaving taxpayers with a mix of modest relief and ongoing pressure.

Let’s look at each type of tax in more detail.

Personal Tax Rates – inflationary adjustment is back

The 2026 Budget introduces inflationary adjustments to tax brackets and rebates, offering welcome relief to taxpayers after two years with no adjustments.

This means that the impact of "bracket creep" - where inflationary salary increases push taxpayers into higher tax brackets - should be reduced. However, the adjustment only applies to this year and does not make up for the effects of the past two years, meaning taxpayers are still not fully caught up.

The tax-free thresholds are expected to increase to approximately:

- R99,000 for taxpayers under 65 years

- R153,250 for taxpayers aged 65 to under 75 years

- R171,300 for taxpayers aged 75 and older

Please click on our updated take-home pay calculator to see your salary for the new tax year.

|

Taxable Income (R) |

Rate of Tax (R) |

|

1 – 245 100 |

18% of taxable income |

|

245 101 – 383 100 |

44 118 + 26% of taxable income above 245 100 |

|

383 101 – 530 200 |

79 998 + 31% of taxable income above 383 100 |

|

530 201 – 695 800 |

125 599 + 36% of taxable income above 530 200 |

|

695 801 – 887 000 |

185 215 + 39% of taxable income above 695 800 |

|

887 001 - 1 878 600 |

259 783+ 41% of taxable income above 887 000 |

|

1 878 601 and above |

666 339 + 45% of taxable income above 1 878 600 |

Capital Gains Tax - some relief

The annual CGT exclusion increases from R40,000 to R50,000, the first increase since 2012, allowing individuals to realise more capital gains tax-free each year.

The primary residence exclusion increases from R2m to R3m providing meaningful tax relief for home owners when selling their primary residence, with potential savings up to R180,000, depending on the size of the gain and the taxpayer's marginal tax rate.

There were no changes to CGT inclusion rates this year. Individuals still have to include 40% of the gain in their income while companies and trusts still have to include 80% of the gain in their income. The overall maximum effective tax rates remain as follows:

- Individuals 18%

- Companies 21,6%

- Trusts 36%

Dividends

The Withholding Tax on Dividends remains the same at 20%.

Donations Tax - increase in annual exemption

The annual donations tax exemption increases from R100,000 to R150,000, while the rates remain unchanged at 20% (and 25% above R30 million). Remember that donations between spouses are still tax free!

Estate Tax

The Estate Duty threshold stays the same - above R3.5m, and up to R30m, estates will be taxed at 20%, and then at a rate of 25% above R30m.

Interest and investment exemptions - tax free contribution increase

The interest exemption thresholds stay at R23,800 for those under 65 years of age and R34,500 for those over 65 and older.

The annual contribution limit for tax-free savings accounts has increased from R36,000 to R46,000. This is the first increase to the annual limit since 2021. The lifetime limit stays at R500,000, so if you contribute the maximum each year, you’ll reach the limit sooner.

Medical Tax Credit –inflation adjustment at last

Similar to the tax brackets, the medical tax credits have also increased in line with inflation. You and your first dependent will be allowed a tax credit of R376 (2026: R364) and thereafter R254 (2026:R246) for all other dependents.

Lump sum payouts and the retirement deduction - maximum cap increase to R430,000

The retirement tax tables for lump sums withdrawn before retirement, and for lump sums withdrawn at retirement remain the same as last year. The once-off tax-free amount of R550,000 that can be withdrawn at retirement remains the same as last year.

The rules for deducting pension, provident, and retirement annuity contributions remain unchanged. You can still deduct up to 27.5% of the greater of your remuneration or taxable income, but the annual maximum cap has increased from R350,000 to R430,000.

Retirement fund lump sum withdrawal benefits

|

Taxable Income (R) |

Rate of Tax (R) |

|

0 - 27 500 |

0% of taxable income |

|

27 501 - 726 000 |

18% of taxable income above 27 500 |

|

726 001 - 1 089 000 |

125 730 + 27% of taxable income above 726 000 |

|

1 089 001 and above |

223 740 + 36% of taxable income above 1 089 000 |

Retirement fund lump sum benefits or severance benefits

|

Taxable Income (R) |

Rate of Tax (R) |

|

0 - 550 000 |

0% of taxable income |

|

550 001 - 770 000 |

18% of taxable income above 550 000 |

|

770 001 - 1 155 000 |

39 600 + 27% of taxable income above 770 000 |

|

1 155 001 and above |

143 550 + 36% of taxable income above 1 155 000 |

Sin Taxes

If you enjoy a drink or a smoke, expect to pay a little more. Excise duties increased in line with inflation by 3.4%, adding roughly 8c to a can of beer or cider, about 15c per bottle of wine, and around R3.20 per bottle of spirits. Cigarettes increase by approximately 77c per pack, and 11c more for vapes.

A small percentage increase, but it adds up - especially if it’s a daily habit.

Fuel levy

Fuel taxes are increasing, adding a few extra cents per litre. The general fuel levy rises by 9c for petrol and 8c for diesel, the carbon levy by 5c (petrol) and 6c (diesel), and the RAF levy by 7c per litre. Small increases individually, but they add up over time.

Small Business Tax -some tax relief and reduced administrative burden

Small Business Corporations (SBC)

The tax free threshold for SBCs has increased from R95,750 to R99,000.

|

Taxable Income (R) |

Rate of Tax (R) |

|

1 – 99 000 |

0% of taxable income |

|

99 001 - 365 000 |

7% of taxable income above 99 000 |

|

365 001 - 550 000 |

18 620 + 21% of taxable income above 365 000 |

|

550 001 and above |

57 470 + 27% of the amount above 550 000 |

Turnover Tax for Micro Businesses

The turnover tax threshold increases from R1 million to R2,3 million, the first adjustment since 2009. This brings the limit more in line with inflation and allows more small businesses to qualify for this simplified tax regime. In addition, there has been a significant increase in all of the turnover tax brackets with the tax free threshold increasing from R335,000 to R600,000.

|

Taxable Income (R) |

Rate of Tax (R) |

|

0 - 600 000 |

0% of taxable income |

|

600 001 - 950 000 |

1% of taxable turnover above 600 000 |

|

950 001 - 1 400 000 |

3 500 + 2% of taxable turnover above 950 000 |

|

1 400 001 and above |

12 500 + 3% of taxable turnover above 1 400 000 |

Corporate Tax

The corporate tax rate will remain at 27% for the year ahead.

VAT Rate

The VAT registration threshold has increased from R1m to R2,3m reducing the compliance burden and allowing more small businesses to stay outside the VAT net.