Turnover Tax Explained

Turnover Tax Explained

Turnover tax

Turnover Tax is a simplified tax system only available to sole proprietors, partnerships, companies or close corporations with a "qualifying turnover" of less than R1m per year. These types of entities are called micro businesses.

As the name implies, Turnover Tax is a type of tax, which is calculated against the turnover of a business, as opposed to a percentage of profit (i.e. income less business expenses) as per usual business tax. This difference reduces the administration burden on business owners as there's less of a need to keep a detailed record of expenses and understand which are deductible for tax purposes.

Turnover tax isn't available for just any business, though, and you'll have to meet SARS requirements in order to register.

Let's have a quick look at the qualifying criteria before we go into further detail.

Does my business qualify for turnover tax?

Turnover tax is reserved for micro businesses with a "qualifying turnover" of less than R1 million for the financial year.

"Qualifying turnover" is the total amount received by a business for the year of assessment from carrying on business activities. For the purpose of determining the R1 million cap, the following amounts will be excluded from qualifying turnover:

- All receipts of a capital nature — for example, an amount received from the sale of equipment that was used in the business. This means that even if your turnover was R900,000 for the year and you disposed of a large business asset for R250,000, the capital from the sale will be excluded and your turnover still falls below the R1 million threshold.

- Certain Government grants exempt from income tax in terms of the Income Tax Act.

While the above are basic criteria, there are further scenarios and types of businesses that aren't eligible to register for Turnover Tax. Our handy Turnover Tax decision tree will take you through a number of straightforward questions and let you know instantly whether your business qualifies or not.

I qualify for turnover tax. How do I register?

If your business qualifies for turnover tax and you wish to register (note: this is optional) you need to submit a TT01 form to SARS. Regrettably, the registration for turnover tax is a manual process and the registration must be done by SARS appointment and cannot be done on eFiling.

How do I calculate my "taxable turnover"?

While your qualifying turnover is the amount used to determine whether you're eligible for Turnover Tax, your "taxable turnover" is the amount used to calculate the tax payable. These numbers can differ, depending on your business situation.

"Taxable turnover" is the total income generated by the business as a result of its trading activities, e.g. paid invoices for services delivered, or products supplied plus 50% of all receipts of a capital nature from the disposal of business assets.

In addition, registered companies (not individuals) will need to include all interest from investments, but not dividends.

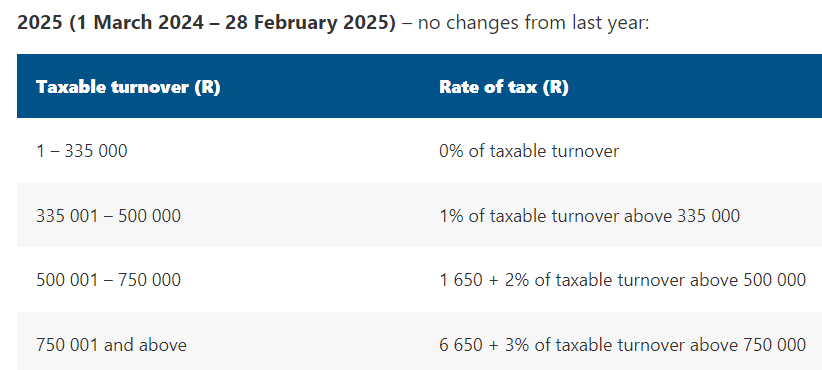

What are the current turnover tax rates?

Below are the Turnover Tax Rates for the years of assessment ending between 1 March 2024 and 28 February 2025:

What about other taxes like capital gains, dividend withholding tax and VAT?

Micro businesses registered for Turnover Tax are exempt from Capital Gains Tax (CGT), however, 50% of the proceeds of business asset sales need to be included in the calculation of your "taxable turnover". Effectively this is a substitute for CGT and ensures that large capital gains aren't routed through the turnover tax system to intentionally avoid CGT.

Registered Turnover Taxpayers are also exempt from Dividend Withholding Tax (DWT) on dividend distributions up to R200,000 per year. Dividends in excess of R200,000 are subject to DWT at the standard rate of 20%.

Companies only need to register for VAT if the value of their taxable supplies exceeds R1 million in a 12-month period. Micro businesses, which by definition have turnover less than R1 million, will therefore not need to register for VAT.

How do I submit returns and pay turnover tax?

Micro businesses registered for turnover tax must prepare two provisional returns per year to support their provisional payments. TT02 in August and February, and a final tax return, TT03, per year. The provisional returns are based on estimated turnover for the year with actual turnover calculated when the final tax return (TT03) is submitted and the taxpayer is assessed.

The TT02 payment advice is the taxpayer's record and does not need to be submitted to SARS. Only the TT03 must be submitted to SARS.

Turnover Taxpayers aren't able to file and pay taxes via eFiling. The TT03 return must be manually submitted via a SARS appointment. This is a consideration point before deciding to register for Turnover Tax (remember, it's optional) as what should be a reduced administrative process, may actually result in a cumbersome one if you have to factor in a long wait for a SARS appointment and other potential delays due to a more manual process.

What records does a micro business registered for turnover tax need to keep?

While Turnover Taxpayers needn't maintain exhaustive records of all business income and expenditure (although this is generally good practice for businesses anyway), SARS does require you to keep the following:

- Records of all amounts received

- Records of dividends declared

- A list of each asset with a cost price of more than R10,000 at the end of the year of assessment, as well as liabilities exceeding R10,000

What if my business exceeds R1m turnover?

Firstly, great job on the booming business!

Secondly, within 21 days of your business breaking the R1 million turnover mark (in a single tax year), you'll need to de-register from Turnover Tax by notifying SARS. As per the registration process, this has to be done in person at a SARS branch.