Individual tax rate tables

By Patrick Knight · Updated

The 2026 Budget introduces inflationary adjustments to 2027 tax brackets and rebates, offering welcome relief to taxpayers after two years with no adjustments.

Please click on our updated take-home pay calculator to see your salary for the new tax year.

|

Taxable Income (R) |

Rate of Tax (R) |

|

1 – 245 100 |

18% of taxable income |

|

245 101 – 383 100 |

44 118 + 26% of taxable income above 245 100 |

|

383 101 – 530 200 |

79 998 + 31% of taxable income above 383 100 |

|

530 201 – 695 800 |

125 599 + 36% of taxable income above 530 200 |

|

695 801 – 887 000 |

185 215 + 39% of taxable income above 695 800 |

|

887 001 - 1 878 600 |

259 783+ 41% of taxable income above 887 000 |

|

1 878 601 and above |

666 339 + 45% of taxable income above 1 878 600 |

2026 tax year (1 March 2025 - 28 Feb 2026) same as 2025 tax year, no changes.

2025 tax year (1 March 2024 - 28 Feb 2025) same as 2024 tax year, no changes.

2024 tax year (1 March 2023 - 28 February 2024) - see changes from last year

2023 tax year (1 March 2022 - 28 February 2023) - see changes from last year

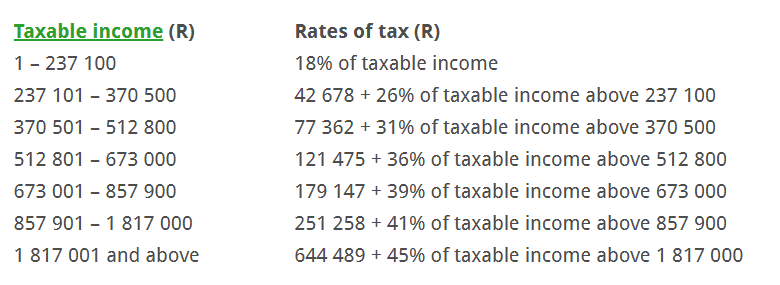

| ​Taxable income (R) | ​Rates of tax (R) |

|---|---|

| 1 – 226 000 | 18% of taxable income |

| 226 001 – 353 100 | 40 680 + 26% of taxable income above 226 000 |

| 353 101 – 488 700 | 73 726 + 31% of taxable income above 353 100 |

| 488 701 – 641 400 | 115 762 + 36% of taxable income above 488 700 |

| 641 401 – 817 600 | 170 734 + 39% of taxable income above 641 400 |

| 817 601 – 1 731 600 | 239 452 + 41% of taxable income above 817 600 |

| 1 731 601 and above | 614 192 + 45% of taxable income above 1 731 600 |

| ​Taxable income (R) | ​Rates of tax (R) |

|---|---|

| 1 – 216 200 | 18% of taxable income |

| 216 200 – 337 800 | 38 916 + 26% of taxable income above 216 200 |

| 337 801 – 467 500 | 70 532 + 31% of taxable income above 337 800 |

| 467 501 – 613 600 | 110 739 + 36% of taxable income above 467 500 |

| 613 601 – 782 200 | 163 335 + 39% of taxable income above 613 600 |

| 782 201 – 1 656 600 | 229 089 + 41% of taxable income above 782 200 |

| 1 656 601 and above | 587 593 + 45% of taxable income above 1 656 600 |

| ​Taxable income (R) | ​Rates of tax (R) |

|---|---|

| 1 – 205 900 | 18% of taxable income |

| 205 901 – 321 600 | 37 062 + 26% of taxable income above 205 900 |

| 321 601 – 445 100 | 67 144 + 31% of taxable income above 321 600 |

| 445 101 – 584 200 | 105 429 + 36% of taxable income above 445 100 |

| 584 201 – 744 800 | 155 505 + 39% of taxable income above 584 200 |

| 744 801 – 1 577 300 | 218 139 + 41% of taxable income above 744 800 |

| 1 577 301 and above | 559 464 + 45% of taxable income above 1 577 300 |

2020 tax year (1 March 2019 - 29 February 2020) - no changes from last year

| Taxable income (R) | Rates of tax (R) |

|---|---|

| 0 – 195 850 | 18% of taxable income |

| 195 851 – 305 850 | 35 253 + 26% of taxable income above 195 850 |

| 305 851 – 423 300 | 63 853 + 31% of taxable income above 305 850 |

| 423 301 – 555 600 | 100 263 + 36% of taxable income above 423 300 |

| 555 601 – 708 310 | 147 891 + 39% of taxable income above 555 600 |

| 708 311 – 1 500 000 | 207 448 + 41% of taxable income above 708 310 |

| 1 500 001 and above | 532 041 + 45% of taxable income above 1 500 000 |

2019 tax year (1 March 2018 - 28 February 2019) - see changes from last year

| Taxable income (R) | Rates of tax (R) |

|---|---|

| 0 – 195 850 | 18% of taxable income |

| 195 851 – 305 850 | 35 253 + 26% of taxable income above 195 850 |

| 305 851 – 423 300 | 63 853 + 31% of taxable income above 305 850 |

| 423 301 – 555 600 | 100 263 + 36% of taxable income above 423 300 |

| 555 601 – 708 310 | 147 891 + 39% of taxable income above 555 600 |

| 708 311 – 1 500 000 | 207 448 + 41% of taxable income above 708 310 |

| 1 500 001 and above | 532 041 + 45% of taxable income above 1 500 000 |

| Taxable income (R) | Rates of tax (R) |

|---|---|

| 0 – 189 880 | 18% of taxable income |

| 189 881 – 296 540 | 34 178 + 26% of taxable income above 189 880 |

| 296 541 – 410 460 | 61 910 + 31% of taxable income above 296 540 |

| 410 461 – 555 600 | 97 225 + 36% of taxable income above 410 460 |

| 555 601 – 708 310 | 149 475 + 39% of taxable income above 555 600 |

| 708 311 – 1 500 000 | 209 032 + 41% of taxable income above 708 310 |

| 1 500 001 and above | 533 625 + 45% of taxable income above 1 500 000 |

2017 tax year (1 March 2016 - 28 February 2017)

| Taxable income (R) | Rates of tax (R) |

|---|---|

| 0 – 188 000 | 18% of taxable income |

| 188 001 – 293 600 | 33 840 + 26% of taxable income above 188 000 |

| 293 601 – 406 400 | 61 296 + 31% of taxable income above 293 600 |

| 406 401 – 550 100 | 96 264 + 36% of taxable income above 406 400 |

| 550 101 – 701 300 | 147 996 + 39% of taxable income above 550 100 |

| 701 301 and above | 206 964 + 41% of taxable income above 701 300 |

Tax Rebates

| Primary | Secondary | Tertiary | |

| (Under 65) | (65 and older) | (75 and older) | |

| 2027 | R17 820 | R9 765 | R3 249 |

| 2026 | R 17 235 | R 9 444 | R 3 145 |

| 2025 | R 17 235 | R 9 444 | R 3 145 |

| 2024 | R 17 235 | R 9 444 | R 3 145 |

| 2023 | R 16 425 | R 9 000 | R 2 997 |

| 2022 | R 15 714 | R 8 613 | R 2 871 |

| 2021 | R 14 958 | R 8 199 | R 2 736 |

| 2020 | R 14 220 | R 7 794 | R 2 601 |

| 2019 | R 14 067 | R 7 713 | R 2 574 |

| 2018 | R 13 635 | R 7 479 | R 2 493 |

| 2017 | R 13 500 | R 7 407 | R 2 466 |

Tax Thresholds

| Under 65 | 65 and older | 75 and older | |

| 2027 | R99 000 | R153 250 | R171 300 |

| 2026 | R 95 750 | R 148 217 | R 165 689 |

| 2025 | R 95 750 | R 148 217 | R 165 689 |

| 2024 | R 95 750 | R 148 217 | R 165 689 |

| 2023 | R 91 250 | R 141 250 | R 157 900 |

| 2022 | R 87 300 | R 135 150 | R 151 100 |

| 2021 | R 83 100 | R 128 650 | R 143 850 |

| 2020 | R 79 000 | R 122 300 | R 136 750 |

| 2019 | R 78 150 | R 121 000 | R 135 300 |

| 2018 | R 75 750 | R 117 300 | R 131 150 |

| 2017 | R 75 000 | R 116 150 | R 129 850 |